The BRICS+ bloc (initially comprising Brazil, Russia, India, China, and South Africa) was established in 2006 on the premise that the world needed a balance to counter of dominance of Western powers. It can effectively be thought of as a version of the ‘Group of Seven (G7)’ for developing economies.

After little initial fanfare, the bloc has evolved into a significant player in the global economic arena via the coordination of its members’ economic and diplomatic policies and the founding of new financial institutions. Institutions such as the New Development Bank (NDB) and the Contingent Reserve Arrangement (CRA) have been developed to replicate the World Bank and International Monetary Fund (IMF) respectively, albeit they are considerably smaller that this stage.

Representing over half of the world’s population and rapidly approaching parity with the G7 in terms of economic output, understanding the scale of BRICS+ and its influence on international trade and finance is crucial for investors, now and in the years to come. This article explores the expanding dynamics of BRICS+, highlighting the emerging investment opportunities that may arise from these shifts.

Timeline

Demographics

The BRICS+ bloc’s expanding population is likely to significantly influence global consumer demands and market dynamics. The combined population of BRICS+ has reached approximately 3.9 billion, representing around 48% [1] of the world’s population, and the increasing middle class in these regions is likely to drive demand for a wide range of goods and services, reshaping global markets.

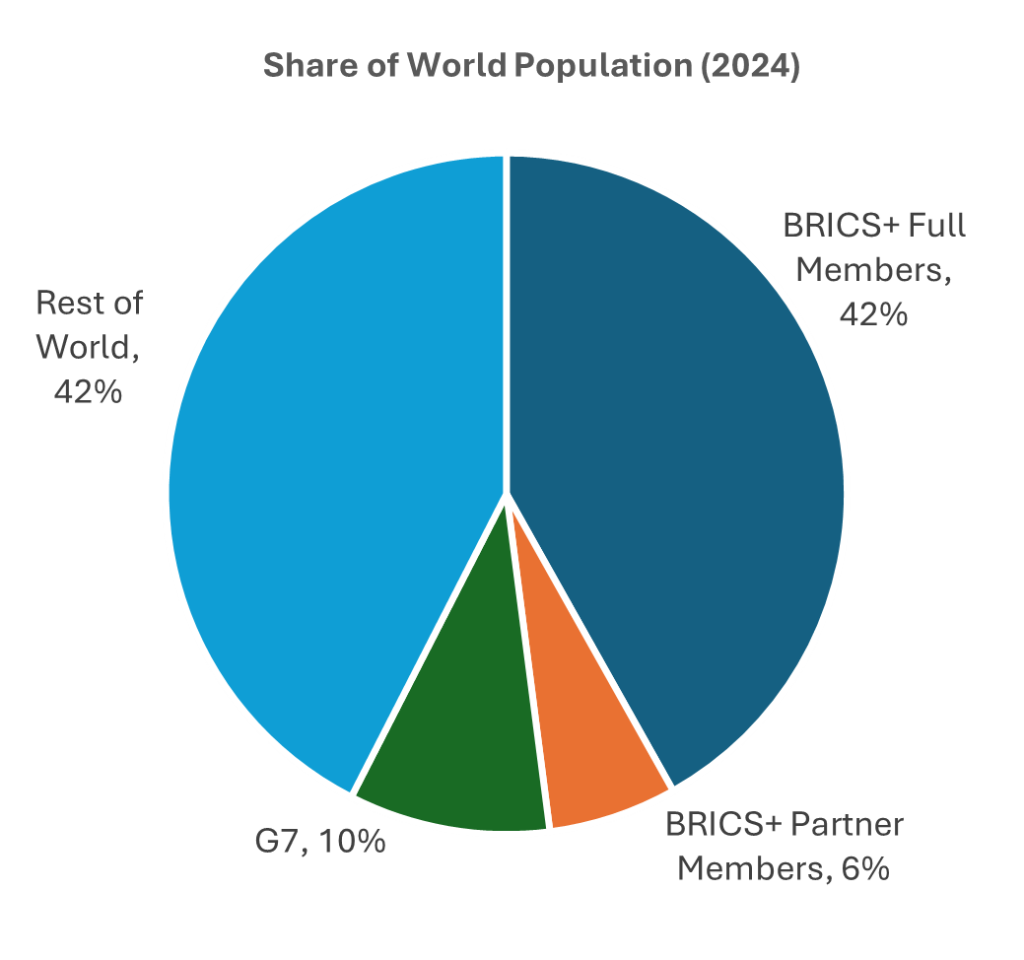

The chart below illustrates the substantial population base (i.e. consumers) of BRICS+ as a share of the world’s 8.2 billion people, compared to those of the G7 countries (Canada, France, Germany, Italy, Japan, the United Kingdom and the United States) and the Rest of World (ROW) [2].

In addition to the aggregate population comparison, the demographic composition of the BRICS+ bloc is also a critical factor in understanding its potential growth and benefit to investors. The bloc’s unique demographic advantage—characterised by a younger population compared to the aging G7—positions it favourably for future economic growth and consumer market expansion. With an average age of 42, the G7 population is almost 10 years older than that of BRICS+ at 32 [3]. As outlined in the table below, future demographic projections show BRICS+ members accounting for an even bigger share of the global population over the next 2 decades [4] [5].

| BRICS + (Full & Partner Members) | G7 | |

|---|---|---|

|

Average Birth Rate |

1.87 |

1.47 |

|

Projected Population: 2030 |

4 billion |

800 million |

|

Projected Population: 2050 |

4.5 billion |

700 million |

The demographic advantage of the BRICS+ nations will not come without its growing pains as populations increasingly shift to the middle class and require significantly more infrastructure and social services. However, recent developments in technology and AI can potentially fast-track this transition – a phenomenon referred to as ‘leapfrogging’, where countries with underdeveloped technology or economic bases are able to bypass traditional stages of development quickly by adopting modern systems. As an example, in telecommunications, countries such as India, Ghana and Nigeria have almost completely skipped the adoption of landlines and have gone straight to mobile [6].

We think this dynamic is only just beginning in emerging countries while countries such as the UK and the US struggle with aging infrastructure and massive costs to upgrade or replace existing power and energy transmission facilities. In comparison, as of July 2024, there were 59 nuclear reactors under construction worldwide with BRICS+ nations (including Turkey) building 40 of them [7]. BRICS+ members are also at the cutting edge of this technology with China planning to build the world’s first-ever nuclear power station using molten salt as the fuel carrier and coolant, and thorium as a fuel source.

Economic Power

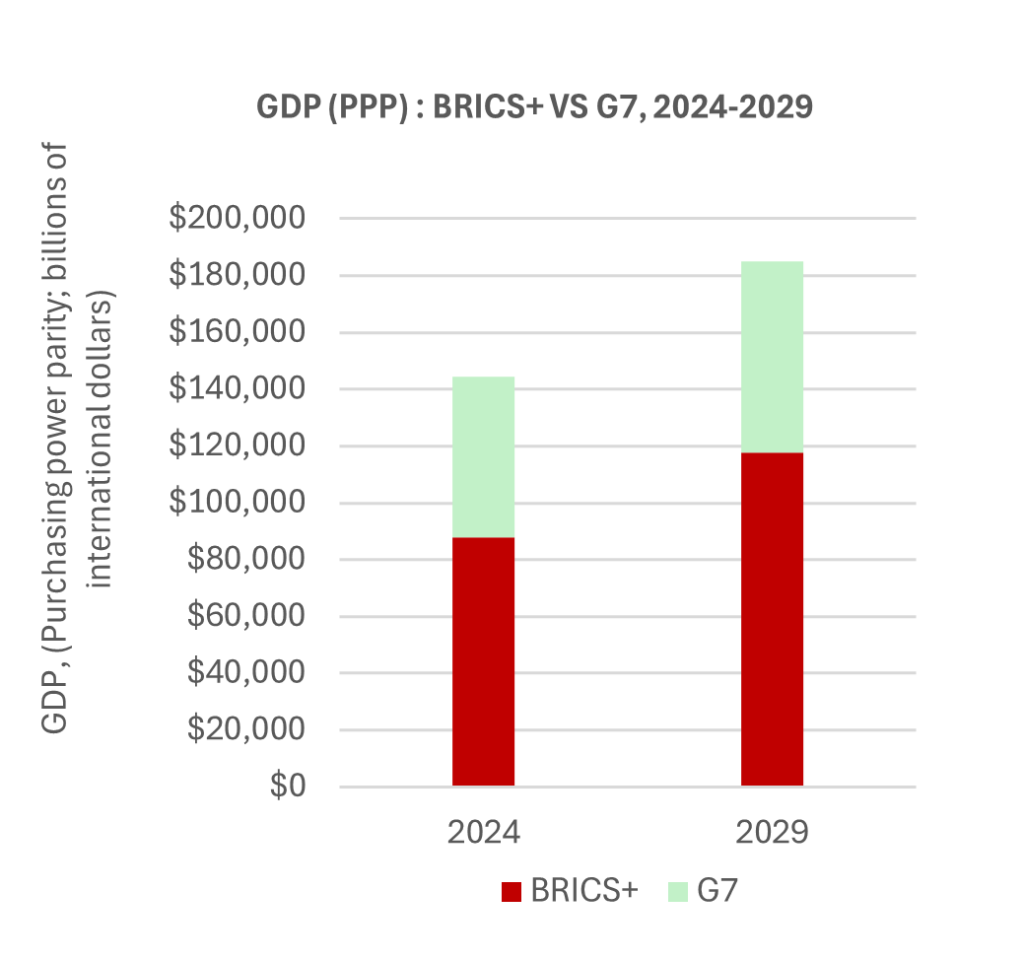

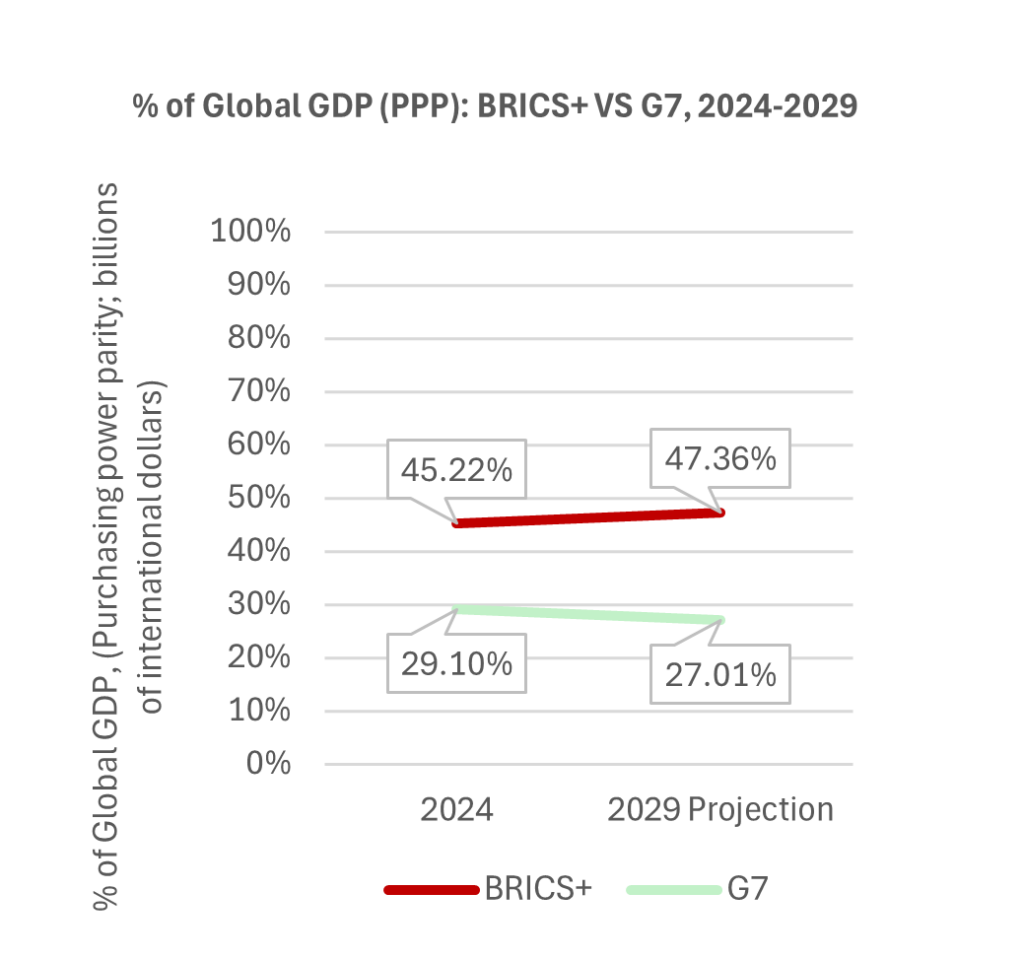

As seen in the charts below, BRICS+ member countries contributed 45.22% of global GDP (adjusted for purchasing power parity) in 2024, compared to just 29.08% for the G7 countries [8].

By 2029, IMF forecasts suggest the gap will widen further, and that is assuming BRICS+ membership stays static, something the recent designation of ‘partner countries’ suggests is unlikely. An additional 20+ countries have also made initial steps to become a member of BRICS+. If the group is expanded to 30-40 members over the next few years, it is highly probable that its contribution to global GDP will surpass 50% before 2030.

Financial Market Shifts

The increasing economic clout of BRICS+ presents a paradigm shift in global financial markets, driven by macroeconomic trends including rapid urbanisation, robust employment growth and rising disposable incomes. We believe investors should see these changes to the current global financial system as an overall positive, increasing trade and employment opportunities across countries that represent the majority of the world’s population. This is likely to drive rising disposable income and consumption growth over the long-term, offering investment opportunities in BRICS+ facing companies providing consumer products and services.

The movement to reduce the primacy of the U.S. dollar in international trade (de-dollarisation) is a major development but will likely be a slow process. It is gaining momentum, with BRICS nations actively seeking to reduce reliance on the US Dollar and shifting towards local currency settlement with gold as a net trade balancing item, but as the US dollar is still used in over 80% of global trade, this move will take considerable time.

From a structural perspective, the group has made a commitment to launch a blockchain-based trade and payments platform that would substantially reduce the cost of transactions between member countries, encouraging the expansion of trade through lowering costs and permitting the use of local currencies in transactions by members. This is a direct challenge to the continued dominance of the US-based SWIFT payment system used by banks globally today.

Further initiatives like the creation of BRICSClear, which would act as a trade clearing, settlement and custody platform for financial asset trading between member states, an alternative to the current global leader EuroClear. The need for secure asset custody is seen as critical by members of the bloc to ensure BRICS+ assets are not confiscated by G7 members, particularly following the confiscation of US$300 billion of Russian central bank assets in 2022 following the invasion of Ukraine.

Sectors to Consider

Understanding BRICS+ is not just about observing geopolitical changes; it’s about identifying actionable insights that can inform investment strategies in a rapidly evolving financial landscape. By recognising the trends within this coalition, investors can better position themselves to capitalise on economic growth and potential investment opportunities in developing markets.

As BRICS+ nations collectively enhance their GDP, they are poised to reshape consumer demand patterns, with potential beneficiaries including the following sectors:

Conclusion

Understanding the evolving landscape of the BRICS+ bloc is essential for investors aiming to navigate the complexities of global markets. The significant demographic advantages and rapid economic growth within BRICS+ member countries, operating together under a common rules-based BRICS trading framework, should drive faster GDP, growth in consumer spending and a thriving environment for growing companies.

While excellent opportunities exist across the world, allocations to BRICS+ nations – particularly those in Asia – remain relatively low. We think that selectively including industry leading companies that can benefit from the overall growth of the bloc can add uncorrelated alpha to investment portfolios over the medium term.

At Carrara, we manage a truly global portfolio across both developed and developing markets. We welcome any further discussions of our thematic ideas, stockholdings, or macro thinking – please contact us for more information.

Citations

[1], [2] https://database.earth/population/by-country/2024

[3] https://www.worldometers.info/world-population/population-by-country/

[4] https://www.cia.gov/the-world-factbook/field/median-age/country-comparison

[5] https://worldpopulationreview.com/

[6] https://www.csis.org/analysis/need-leapfrog-strategy

[7] https://www.statista.com/statistics/513671/number-of-under-construction-nuclear-reactors-worldwide/